Financial Toolbox

Analyze financial data and develop financial models

Have questions? Contact Sales.

Have questions? Contact Sales.

Financial Toolbox provides functions for the mathematical modeling and statistical analysis of financial data. You can analyze, backtest, and optimize investment portfolios taking into account turnover, transaction costs, semi-continuous constraints, and minimum or maximum number of assets. The toolbox enables you to estimate risk, model credit scorecards, analyze yield curves, price fixed-income instruments and European options, and measure investment performance.

Stochastic differential equation (SDE) tools let you model and simulate a variety of stochastic processes. Time series analysis functions let you perform transformations or regressions with missing data and convert between different trading calendars and day-count conventions.

Compute technical indicators (including moving averages, momentums, oscillators, volume indicators, and rate of change) and create financial charts (including candlestick, open-high-low-close, and Bollinger band charts).

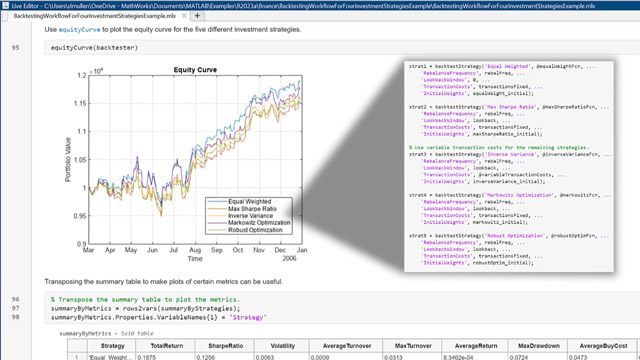

Evaluate investment performance using built-in functions for calculating metrics such as Sharpe ratio, information ratio, tracking error, risk-adjusted return, sample lower partial moments, expected lower partial moments, maximum drawdown, and expected maximum drawdown.

Perform mean-variance, mean absolute deviation (MAD), and conditional value at risk (CVaR) portfolio optimizations.

Estimate the efficient portfolio and its weights that maximize Sharpe ratio, visualize efficient frontiers, and calculate portfolio risks, including portfolio standard deviation, MAD, VaR, and CVaR.

Apply portfolio optimization constraints, including tracking error, linear inequality, linear equality, bound, budget, group, group ratio, average turnover, one-way turnover, minimum number of assets, and maximum number of assets. Incorporate proportional or fixed transaction costs on either gross or net portfolio return optimization.

Define investment strategies and use the backtesting framework to run backtests, analyze results, and generate performance metrics for your strategies from historical or simulated market data. Incorporate technical indicators, sentiment, and other trading signals into your strategies. The framework also supports custom transaction costs, expanding or rolling lookback windows, margin trading, and long/short portfolios.

Use Financial Toolbox to calculate present and future values; determine nominal, effective, and modified internal rates of return; calculate amortization and depreciation; and determine the periodic interest rate paid on loans or annuities.

Calculate price, yield-to-maturity, duration, and convexity of fixed-income securities. Compute analytics such as complete cash flow date, cash flow amounts, and time-to-cash-flow mapping for bonds. Calculate option prices and greeks using Black and Black-Scholes formulas.

Generate random variables for Monte Carlo simulations based on a variety of SDE models, including Brownian motion, geometric Brownian motion, constant elasticity of variance, Cox-Ingersoll-Ross, Hull-White/Vasicek, and Heston.

“MATLAB and MATLAB Compiler SDK enabled us to rapidly deliver a sophisticated portfolio analytics web application with confidence that it will return accurate results extremely quickly, ensuring a highly usable and stable platform for our clients.”

Lee Eriera, Frontier Advisors

You can also select a web site from the following list

Americas

Europe

Asia Pacific