Credit Scorecard Modeling Using Observation Weights

When creating a creditscorecard object, the table used

for the input data argument either defines or does not define

observational weights. If the data does not use weights, then the

"counts" for Good, Bad, and

Odds are used by credit score card functions. However, if the

optional WeightsVar argument is specified when creating a

creditscorecard object, then the "counts" for

Good, Bad, and Odds are the

sum of weights.

For example, here is a snippet of an input table that does not define observational weights:

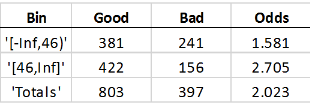

If you bin the customer age predictor data, with customers up to 45 years old in one bin, and 46 and up in another bin, you get these statistics:

Good means the total number of rows with a 0

value in the status response variable. Bad the

number of 1’s in the status column.

Odds is the ratio of Good to

Bad. The Good, Bad, and

Odds is reported for each bin. This means that there are 381

people in the sample who are 45 and under who paid their loans, 241 in the same age

range who defaulted, and therefore, the odds of being good for that age range is

1.581.

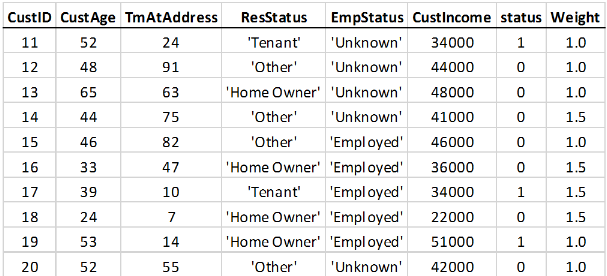

Suppose that the modeler thinks that people 45 and younger are underrepresented in

this sample. The modeler wants to give all rows with ages up to 45 a higher weight.

Assume that the modeler thinks the up to 45 age group should have 50% more weight than

rows with ages 46 and up. The table data is expanded to include the observation weights.

A Weight column is added to the table, where all rows with ages 45

and under have a weight of 1.5, and all other rows a weight of

1. There are other reasons to use weights, for example, recent

data points may be given higher weights than older data points.

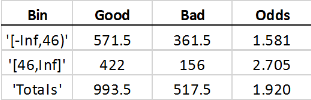

If you bin the weighted data based on age (45 and under, versus 46 and up) the

expectation is that each row with age 45 and under must count as 1.5 observations, and

therefore the Good and Bad “counts” are increased

by 50%:

The “counts” are now “weighted frequencies” and are no longer integer values. The

Odds do not change for the first bin. The particular weights

given in this example have the effect of scaling the total Good and

Bad counts in the first bin by the same scaling factor, therefore

their ratio does not change. However, the Odds value of the total

sample does change; the first bin now carries a higher weight, and because the odds in

that bin are lower, the total Odds are now lower, too. Other credit

scorecard statistics not shown here, such as WOE and

Information Value are affected in a similar way.

In general, the effect of weights is not simply to scale frequencies in a particular bin, because members of that bin will have different weights. The goal of this example is to demonstrate the concept of switching from counts to the sum of weights.

See Also

creditscorecard | autobinning | bininfo | fitmodel | validatemodel