simulateNormalScenariosByData

Simulate multivariate normal asset return scenarios from data

Syntax

Description

obj = simulateNormalScenariosByData(obj,AssetReturns)PortfolioCVaR or PortfolioMAD

objects. For details on the workflows, see PortfolioCVaR Object Workflow,

and PortfolioMAD Object Workflow.

obj = simulateNormalScenariosByData(obj,AssetReturns,NumScenarios,Name,Value)PortfolioCVaR or PortfolioMAD

objects using additional options specified by one or more

Name,Value pair arguments.

This function estimates the mean and covariance of asset returns from either

price or return data and then uses these estimates to generate the specified

number of scenarios with the function mvnrnd.

Data can be in a NumSamples-by-NumAssets

matrix of NumSamples prices or returns at a given periodicity

for a collection of NumAssets assets, a table or a timetable.

Note

If you want to use the method multiple times and you want to simulate

identical scenarios each time the function is called, precede each

function call with rng(seed) using a specified integer

seed.

Examples

Given a PortfolioCVaR object p, use the simulateNormalScenariosByData function to simulate multivariate normal asset return scenarios from data.

m = [ 0.05; 0.1; 0.12; 0.18 ];

C = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

m = m/12;

C = C/12;

RawData = mvnrnd(m, C, 240);

NumScenarios = 2000;

p = PortfolioCVaR;

p = simulateNormalScenariosByData(p, RawData, NumScenarios)p =

PortfolioCVaR with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

ProbabilityLevel: []

Turnover: []

BuyTurnover: []

SellTurnover: []

NumScenarios: 2000

Name: []

NumAssets: 4

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: []

UpperBound: []

LowerBudget: []

UpperBudget: []

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

p = setDefaultConstraints(p); p = setProbabilityLevel(p, 0.9); disp(p);

PortfolioCVaR with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

ProbabilityLevel: 0.9000

Turnover: []

BuyTurnover: []

SellTurnover: []

NumScenarios: 2000

Name: []

NumAssets: 4

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [4×1 double]

UpperBound: []

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: [4×1 categorical]

To illustrate using the simulateNormalScenariosByData function with AssetReturns data continued in a timetable object, use the CAPMuniverse.mat which contains a timetable object (AssetTimeTable) for returns data.

load CAPMuniverse;

AssetsTimeTable.Propertiesans =

TimetableProperties with properties:

Description: ''

UserData: []

DimensionNames: {'Time' 'Variables'}

VariableNames: {'AAPL' 'AMZN' 'CSCO' 'DELL' 'EBAY' 'GOOG' 'HPQ' 'IBM' 'INTC' 'MSFT' 'ORCL' 'YHOO' 'MARKET' 'CASH'}

VariableTypes: ["double" "double" "double" "double" "double" "double" "double" "double" "double" "double" "double" "double" "double" "double"]

VariableDescriptions: {}

VariableUnits: {}

VariableContinuity: []

RowTimes: [1471×1 datetime]

StartTime: 03-Jan-2000

SampleRate: NaN

TimeStep: NaN

Events: []

CustomProperties: No custom properties are set.

Use addprop and rmprop to modify CustomProperties.

head(AssetsTimeTable,5)

Time AAPL AMZN CSCO DELL EBAY GOOG HPQ IBM INTC MSFT ORCL YHOO MARKET CASH

___________ _________ _________ _________ _________ _________ ____ _________ _________ _________ _________ _________ _________ _________ __________

03-Jan-2000 0.088805 0.1742 0.008775 -0.002353 0.12829 NaN 0.03244 0.075368 0.05698 -0.001627 0.054078 0.097784 -0.012143 0.00020522

04-Jan-2000 -0.084331 -0.08324 -0.05608 -0.08353 -0.093805 NaN -0.075613 -0.033966 -0.046667 -0.033802 -0.0883 -0.067368 -0.03166 0.00020339

05-Jan-2000 0.014634 -0.14877 -0.003039 0.070984 0.066875 NaN -0.006356 0.03516 0.008199 0.010567 -0.052837 -0.073363 0.011443 0.00020376

06-Jan-2000 -0.086538 -0.060072 -0.016619 -0.038847 -0.012302 NaN -0.063688 -0.017241 -0.05824 -0.033477 -0.058824 -0.10307 0.011743 0.00020266

07-Jan-2000 0.047368 0.061013 0.0587 -0.037708 -0.000964 NaN 0.028416 -0.004386 0.04127 0.013091 0.076771 0.10609 0.02393 0.00020157

Notice that GOOG has missing data (NaN) because it was not listed before Aug 2004. The simulateNormalScenariosByData function has a name-value pair argument 'MissingData' that indicates with a Boolean value whether to use the missing data capabilities of Financial Toolbox™ software. The default value for 'MissingData' is false which removes all samples with NaN values. If, however, 'MissingData' is set to true, the estimateAssetMoments function uses the ECM algorithm to estimate asset moments. The simulateNormalScenariosByData function also accepts a name-value pair argument 'DataFormat' with a corresponding value set to 'prices' to indicate that the input to the function is in the form of asset prices and not returns (the default value for the 'DataFormat' argument is 'returns').

NumScenarios = 100; r = PortfolioCVaR; r = simulateNormalScenariosByData(r,AssetsTimeTable,NumScenarios,'DataFormat','Returns','MissingData',true);

In addition, simulateNormalScenariosByData extracts asset names or identifiers from a timetable object when the name-value argument 'GetAssetList' is set to true (its default value is false). If the 'GetAssetList' value is true, the timetable column identifiers are used to set the AssetList property of the PortfolioCVaR object. To show this, the formation of the PortfolioCVaR object r is repeated with the 'GetAssetList' flag set to true.

r = simulateNormalScenariosByData(r,AssetsTimeTable,NumScenarios,'GetAssetList',true);

disp(r.AssetList) {'AAPL'} {'AMZN'} {'CSCO'} {'DELL'} {'EBAY'} {'GOOG'} {'HPQ'} {'IBM'} {'INTC'} {'MSFT'} {'ORCL'} {'YHOO'} {'MARKET'} {'CASH'}

Create a PortfolioCVaR object p and use the simulateNormalScenariosByData function with market data loaded from CAPMuniverse.mat to simulate multivariate normal asset return scenarios. The market data, AssetsTimeTable, is a timetable of asset returns.

load CAPMuniverse p = PortfolioCVaR('AssetList',Assets); disp(p);

PortfolioCVaR with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

ProbabilityLevel: []

Turnover: []

BuyTurnover: []

SellTurnover: []

NumScenarios: []

Name: []

NumAssets: 14

AssetList: {'AAPL' 'AMZN' 'CSCO' 'DELL' 'EBAY' 'GOOG' 'HPQ' 'IBM' 'INTC' 'MSFT' 'ORCL' 'YHOO' 'MARKET' 'CASH'}

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: []

UpperBound: []

LowerBudget: []

UpperBudget: []

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: []

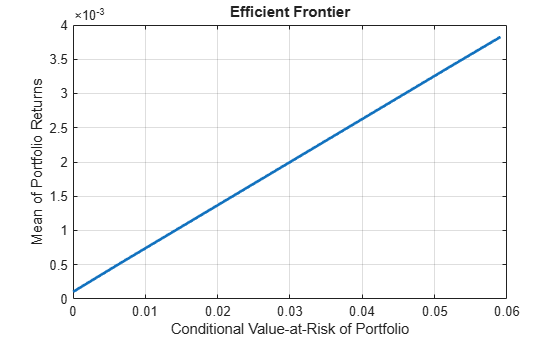

Simulate the scenarios from the timetable data for each of the assets from CAPMuniverse.mat and plot the efficient frontier.

p = simulateNormalScenariosByData(p,AssetsTimeTable,10000,'missingdata',true);

p = setDefaultConstraints(p);

p = setProbabilityLevel(p, 0.9);

plotFrontier(p);

Given a PortfolioMAD object p, use the simulateNormalScenariosByData function to simulate multivariate normal asset return scenarios from data.

m = [ 0.05; 0.1; 0.12; 0.18 ];

C = [ 0.0064 0.00408 0.00192 0;

0.00408 0.0289 0.0204 0.0119;

0.00192 0.0204 0.0576 0.0336;

0 0.0119 0.0336 0.1225 ];

m = m/12;

C = C/12;

RawData = mvnrnd(m, C, 240);

NumScenarios = 2000;

p = PortfolioMAD;

p = simulateNormalScenariosByData(p, RawData, NumScenarios);

p = setDefaultConstraints(p);

disp(p); PortfolioMAD with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

Turnover: []

BuyTurnover: []

SellTurnover: []

NumScenarios: 2000

Name: []

NumAssets: 4

AssetList: []

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [4×1 double]

UpperBound: []

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: [4×1 categorical]

Create a PortfolioMAD object p and use the simulateNormalScenariosByData function with market data loaded from CAPMuniverse.mat to simulate multivariate normal asset return scenarios. The market data, AssetsTimeTable, is a timetable of asset returns.

load CAPMuniverse p = PortfolioMAD('AssetList',Assets); disp(p.AssetList');

{'AAPL' }

{'AMZN' }

{'CSCO' }

{'DELL' }

{'EBAY' }

{'GOOG' }

{'HPQ' }

{'IBM' }

{'INTC' }

{'MSFT' }

{'ORCL' }

{'YHOO' }

{'MARKET'}

{'CASH' }

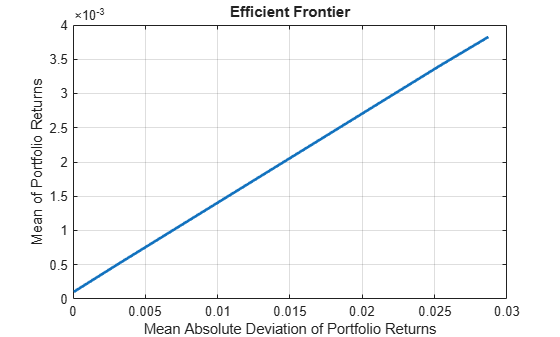

Simulate the scenarios from the timetable data for each of the assets from CAPMuniverse.mat and plot the efficient frontier.

p = simulateNormalScenariosByData(p,AssetsTimeTable,10000,'missingdata',true);

p = setDefaultConstraints(p);

plotFrontier(p);

Input Arguments

Name-Value Arguments

Output Arguments

Tips

You can also use dot notation to simulate multivariate normal asset return scenarios from data for a PortfolioCVaR or PortfolioMAD object.

obj = obj.simulateNormalScenariosByData(AssetReturns,NumScenarios,Name,Value);