Price and Analyze Financial Instruments

This toolbox provides tools to analyze basic fixed-income and derivative instruments. Fixed-income instruments use Securities Industry Association or SIA-compatible analytics for pricing, yield curve modeling, and sensitivity analysis for government, corporate, and municipal fixed-income securities. Derivative instruments use basic Black-Scholes, Black, and binomial option-pricing to compute a standard market model of equity pricing and to calculate the sensitivities of option greeks, such as lambda, theta, and delta. Financial Instruments Toolbox™ supports additional functionality for pricing fixed-income and equity derivative instruments. For more information, see Price Interest-Rate Instruments (Financial Instruments Toolbox) and Price Equity, FX, Commodity, or Energy Instruments (Financial Instruments Toolbox).

Categories

- Analyze Yield Curves

Analyze interest-rate yield curve to determine zero, discount, forward, and par curves

- Price Fixed-Income Instruments

Analyze term structure, interest rates, accrued interest, bond prices, treasury bills, sensitivities, and yields

- Price Derivative Instruments

Analyze equity option valuation and sensitivity

Featured Examples

Hedge Options Using Reinforcement Learning Toolbox

Outperform the traditional BSM approach using an optimal option hedging policy.

Hedge Using Monte Carlo Simulation

Use Monte Carlo simulation to model the probability of different outcomes in a process that cannot easily be predicted due to the intervention of random variables.

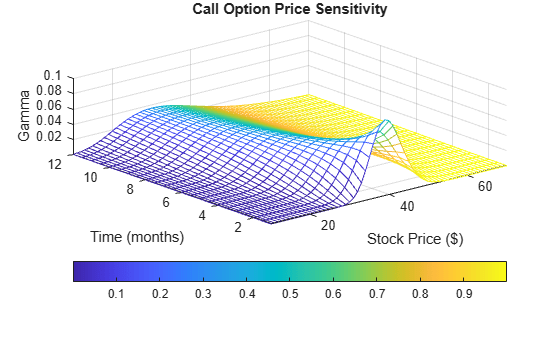

Plotting Sensitivities of an Option

Creates a three-dimensional plot showing how gamma changes relative to price for a Black-Scholes option.

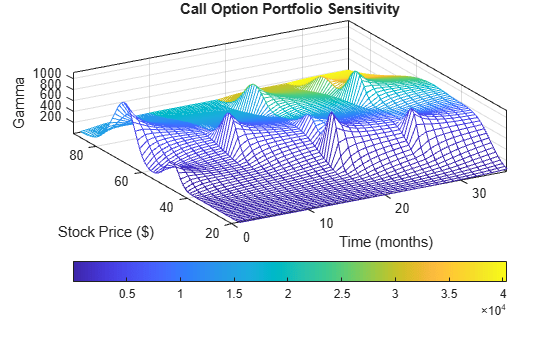

Plotting Sensitivities of a Portfolio of Options

Plots gamma as a function of price and time for a portfolio of ten Black-Scholes options.

Volatility Modeling for Soft Commodities

Demonstrates a diverse set of statistical methods, machine learning techniques, and time-series models that you can apply broadly in the field of volatility modeling. Specifically, this example focuses on the analysis, modeling, and forecasting of volatility within the context of soft commodities.