Impact of Transition Risk on a Mortgage Portfolio

Learn how you can model the impact of climate transition risk on a mortgage loan portfolio and easily gather geographic, climate, and transition data in the same place, translate climate data into financial risk, and create powerful dashboards and reports for quickly assessing the risks and doing deeper dives.

Yannis Ben Ouaghrem, Application Engineering, MathWorks

Published: 27 Feb 2023

Hello, and welcome. This video will show you how you can assess impact of transition risk on the loan portfolio. So calculating transition risk is complex. Assuming we have a portfolio of loans on real estate, to achieve this workflow, we will need to overcome some well known challenges such as-- we will need to gather geographical, climate, transition and financial data at the same place.

Another one could be finding a library that help us to model transition policies and translate them into actual financial metrics, or maybe a last one, we need to have some powerful dashboard and reporting tools to quickly assess the risk and do deep dives into the portfolio.

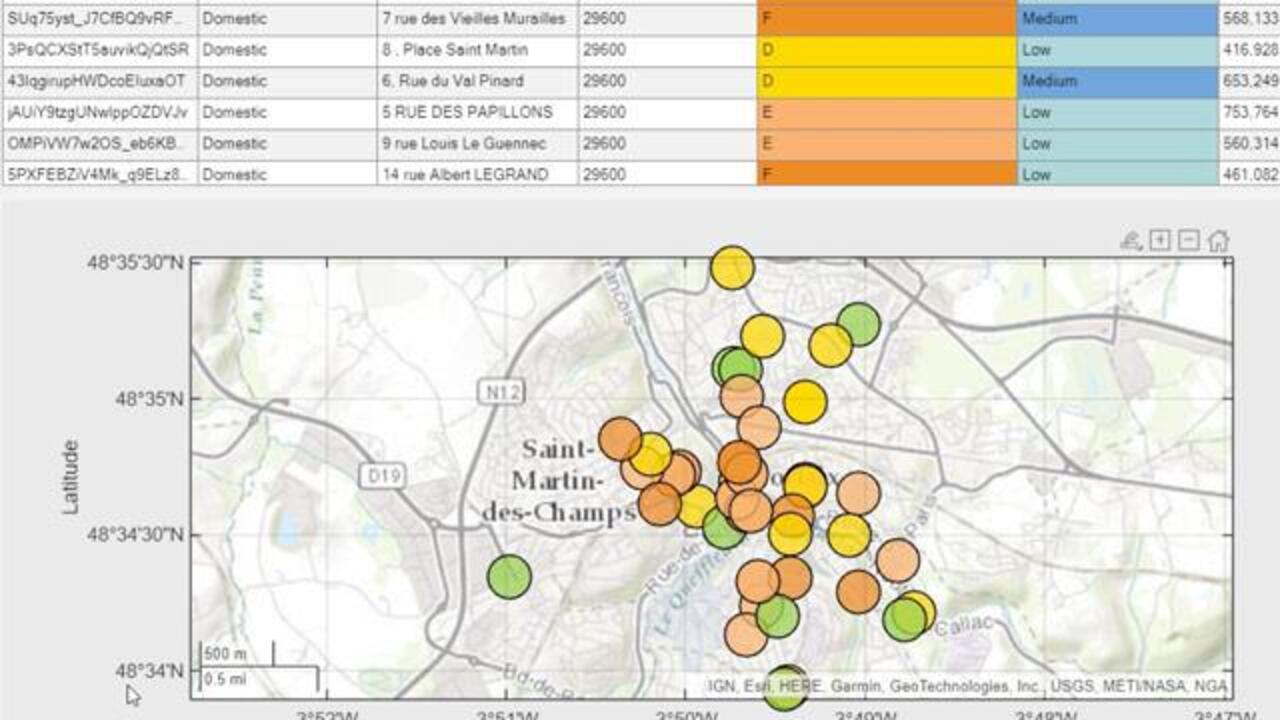

The good news is that the tool like Matlab provides us all that we need and more. OK, let's set the scene and travel to Europe. The European Union created a letter rating that easily indicate had good or bad your residence is in term of energy. With, A, the best rating and, G, the worst one. This rating is called energy performance certificate. Government letters rating, for example, the French one have already enforced climate related laws that oblige landlords to get minimum EPC rating. Otherwise, they will face some consequences that will have a direct impact on their financials.

So let's translate this policy in Matlab. We first need some data. EPC is generally available publicly, simplifying your workflow. Here we will load an Excel file containing information about a portfolio and fetch the EPC rating from a RESTful API, giving us a table with all information wanted. Then we need to protect this data in the future using the policy described at the beginning of the video. This model can be then tuned and used to derive different scenarios.

We can quickly understand what is the actual state of the portfolio, looking at the results shown inside the app. To convert this projected transition to the financial world, we will need to use a cost matrix describing the estimated amount that landlord need to spend to move from one letter to another. Then the asset value of the loan balance can relate this cost based on need.

Looking inside one residence, we can clearly distinguish spikes in the loan to value ratio, describing a transition motivated by the French government climate laws. With this new loan to value ratio projection, we can easily get the probability of default, risk weighted assets, or even the lifetime provisions. And that's it. We successfully assessed the transition risk of our loan portfolio.

Just a quick note. That this use case is a flexible solution, which is adaptable to different geographies, asset type and reporting requirement, which means that I could easily build the same example, as the same floating risk in the UK using the same code, but with different data sources.

All right, if you have any questions or want to discuss the solution do not hesitate to use the comment section. I will be more than happy to learn about your ideas. If you like the content, don't forget to press the like button. Thanks for watching, and see you soon.

Featured Product

Risk Management Toolbox

Up Next:

Related Videos:

Select a Web Site

Choose a web site to get translated content where available and see local events and offers. Based on your location, we recommend that you select: United States.

You can also select a web site from the following list

Americas

- América Latina (Español)

- Canada (English)

- United States (English)

Europe

- Belgium (English)

- Denmark (English)

- Deutschland (Deutsch)

- España (Español)

- Finland (English)

- France (Français)

- Ireland (English)

- Italia (Italiano)

- Luxembourg (English)

- Netherlands (English)

- Norway (English)

- Österreich (Deutsch)

- Portugal (English)

- Sweden (English)

- Switzerland

- United Kingdom (English)