optByHestonNI

Option price by Heston model using numerical integration

Syntax

Description

Price = optByHestonNI(Rate,AssetPrice,Settle,Maturity,OptSpec,Strike,V0,ThetaV,Kappa,SigmaV,RhoSV)

Note

Alternatively, you can use the Vanilla object to price

vanilla options. For more information, see Get Started with Workflows Using Object-Based Framework for Pricing Financial Instruments.

Price = optByHestonNI(___,Name,Value)

Examples

optByHestonNI uses numerical integration to compute option prices and then to plot an option price surface.

Define Option Variables and Heston Model Parameters

AssetPrice = 80;

Rate = 0.03;

DividendYield = 0.02;

OptSpec = 'call';

V0 = 0.04;

ThetaV = 0.05;

Kappa = 1.0;

SigmaV = 0.2;

RhoSV = -0.7;Compute the Option Price for a Single Strike

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 6); Strike = 80; Call = optByHestonNI(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, 'DividendYield', DividendYield)

Call = 4.7007

Compute the Option Prices for a Vector of Strikes

The Strike input can be a vector.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 6); Strike = (76:2:84)'; Call = optByHestonNI(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, 'DividendYield', DividendYield)

Call = 5×1

7.0401

5.8053

4.7007

3.7316

2.8991

Compute the Option Prices for a Vector of Strikes and a Vector of Dates of the Same Lengths

Use the Strike input to specify the strikes. Also, the Maturity input can be a vector, but it must match the length of the Strike vector if the ExpandOutput name-value pair argument is not set to "true".

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, [12 18 24 30 36]); % Five maturities Strike = [76 78 80 82 84]'; % Five strikes Call = optByHestonNI(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, 'DividendYield', DividendYield)

Call = 5×1

8.9560

9.3419

9.6240

9.8560

10.0500

% Five values in vector outputExpand the Output for a Surface

Set the ExpandOutput name-value pair argument to "true" to expand the output into a NStrikes-by-NMaturities matrix. In this case, it is a square matrix.

Call = optByHestonNI(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, 'DividendYield', DividendYield, ... 'ExpandOutput', true) % (5 x 5) matrix output

Call = 5×5

8.9560 10.4543 11.7058 12.8009 13.7728

7.7946 9.3419 10.6337 11.7644 12.7685

6.7244 8.3028 9.6240 10.7828 11.8134

5.7474 7.3378 8.6771 9.8560 10.9074

4.8645 6.4474 7.7930 8.9840 10.0500

Compute the Option Prices for a Vector of Strikes and a Vector of Dates of Different Lengths

When ExpandOutput is "true", NStrikes do not have to match NMaturities (that is, the output NStrikes-by-NMaturities matrix can be rectangular).

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 12*(0.5:0.5:3)'); % Six maturities Strike = (76:2:84)'; % Five strikes Call = optByHestonNI(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, 'DividendYield', DividendYield, ... 'ExpandOutput', true) % (5 x 6) matrix output

Call = 5×6

7.0401 8.9560 10.4543 11.7058 12.8009 13.7728

5.8053 7.7946 9.3419 10.6337 11.7644 12.7685

4.7007 6.7244 8.3028 9.6240 10.7828 11.8134

3.7316 5.7474 7.3378 8.6771 9.8560 10.9074

2.8991 4.8645 6.4474 7.7930 8.9840 10.0500

Compute the Option Prices for a Vector of Strikes and a Vector of Asset Prices

When ExpandOutput is "true", the output can also be a NStrikes-by-NAssetPrices rectangular matrix by accepting a vector of asset prices.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 12); % Single maturity ManyAssetPrices = [70 75 80 85]; % Four asset prices Strike = (76:2:84)'; % Five strikes Call = optByHestonNI(Rate, ManyAssetPrices, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, 'DividendYield', DividendYield, ... 'ExpandOutput', true) % (5 x 4) matrix output

Call = 5×4

3.2944 5.8047 8.9560 12.6052

2.6413 4.8810 7.7946 11.2507

2.0864 4.0575 6.7244 9.9738

1.6230 3.3325 5.7474 8.7783

1.2429 2.7028 4.8645 7.6676

Plot an Option Price Surface

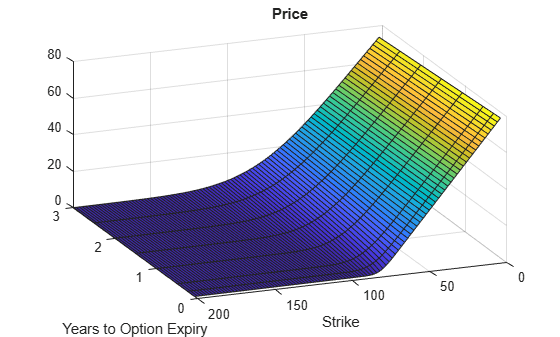

The Strike and Maturity inputs can be vectors. Set ExpandOutput to "true" to output the surface as a NStrikes-by-NMaturities matrix.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 12*[1/12 0.25 (0.5:0.5:3)]'); Times = yearfrac(Settle, Maturity); Strike = (2:2:200)'; Call = optByHestonNI(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, 'DividendYield', DividendYield, ... 'ExpandOutput', true); [X,Y] = meshgrid(Times,Strike); figure; surf(X,Y,Call); title('Price'); xlabel('Years to Option Expiry'); ylabel('Strike'); view(-112,34); xlim([0 Times(end)]); zlim([0 80]);

Input Arguments

Name-Value Arguments

Output Arguments

More About

References

[1] Heston, S. L. “A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options.” The Review of Financial Studies. Vol 6. No. 2. 1993.

[2] Lewis, A. L. “A Simple Option Formula for General Jump-Diffusion and Other Exponential Levy Processes.” Envision Financial Systems and OptionCity.net, 2001.