optSensByBatesFFT

Option price and sensitivities by Bates model using FFT and FRFT

Syntax

Description

[

computes vanilla European option price and sensitivities by Bates model, using Carr-Madan

FFT and Chourdakis FRFT methods.PriceSens,StrikeOut] = optSensByBatesFFT(Rate,AssetPrice,Settle,Maturity,OptSpec,Strike,V0,ThetaV,Kappa,SigmaV,RhoSV,MeanJ,JumpVol,JumpFreq)

Note

Alternatively, you can use the Vanilla object to calculate

price or sensitivities for vanilla options. For more information, see Get Started with Workflows Using Object-Based Framework for Pricing Financial Instruments.

[

adds optional name-value pair arguments. PriceSens,StrikeOut] = optSensByBatesFFT(___,Name,Value)

Examples

Use optSensByBatesFFT to calibrate the FFT strike grid for sensitivities, compute option sensitivities, and plot option sensitivity surfaces.

Define Option Variables and Bates Model Parameters

AssetPrice = 80;

Rate = 0.03;

DividendYield = 0.02;

OptSpec = 'call';

V0 = 0.04;

ThetaV = 0.05;

Kappa = 1.0;

SigmaV = 0.2;

RhoSV = -0.7;

MeanJ = 0.02;

JumpVol = 0.08;

JumpFreq = 2;Compute the Option Sensitivities for the Entire FFT (or FRFT) Strike Grid, Without Specifying "Strike"

Compute option sensitivities and also output the corresponding strikes. If the Strike input is empty ( [] ), option sensitivities will be computed on the entire FFT (or FRFT) strike grid. The FFT (or FRFT) strike grid is determined as exp(log-strike grid), where each column of the log-strike grid has NumFFT points with LogStrikeStep spacing that are roughly centered around each element of log(AssetPrice). The default value for NumFFT is 2^12. In addition to the sensitivities in the first output, the optional last output contains the corresponding strikes.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 6); Strike = []; % Strike is not specified (will use the entire FFT strike grid) % Compute option sensitivities for the entire FFT strike grid [Delta, Kout] = optSensByBatesFFT(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta"); % Show the lowest and highest strike values on the FFT strike grid format MinStrike = Kout(1) % Lowest possible strike in the current FFT strike grid

MinStrike = 2.9205e-135

MaxStrike = Kout(end) % Highest possible strike in the current FFT strike gridMaxStrike = 1.8798e+138

% Show a subset of the strikes and corresponding option sensitivities

Range = (2046:2052);

[Kout(Range) Delta(Range)]ans = 7×2

50.4929 0.9846

58.8640 0.9585

68.6231 0.8498

80.0000 0.5630

93.2631 0.1955

108.7251 0.0319

126.7505 0.0033

Change the Number of FFT (or FRFT) Points and Compare with optSensByBatesNI

Try a different number of FFT (or FRFT) points, and compare the results with numerical integration. Unlike optSensByBatesFFT, which uses FFT (or FRFT) techniques for fast computation across the whole range of strikes, the optSensByBatesNI function uses direct numerical integration and it is typically slower, especially for multiple strikes. However, the values computed by optSensByBatesNI can serve as a benchmark for adjusting the settings for optSensByBatesFFT.

% Try a smaller number of FFT points % (e.g. for faster performance or smaller memory footprint) NumFFT = 2^10; % Smaller than the default value of 2^12 Strike = []; % Strike is not specified (will use the entire FFT strike grid) [Delta, Kout] = optSensByBatesFFT(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta", 'NumFFT', NumFFT); % Compare with numerical integration method Range = (510:516); Strike = Kout(Range); DeltaFFT = Delta(Range); DeltaNI = optSensByBatesNI(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, V0, ... ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta"); Error = abs(DeltaFFT-DeltaNI); table(Strike, DeltaFFT, DeltaNI, Error)

ans=7×4 table

Strike DeltaFFT DeltaNI Error

______ __________ __________ __________

12.696 0.9265 0.99002 0.063524

23.449 0.95153 0.99002 0.038497

43.312 0.95928 0.98928 0.029994

80 0.5355 0.56303 0.027531

147.76 0.0016267 0.00025691 0.0013698

272.93 0.00058267 1.8942e-09 0.00058267

504.11 0.00017752 8.7099e-10 0.00017752

Make Further Adjustments to FFT (or FRFT)

If the values in the output DeltaFFT are significantly different from those in DeltaNI, try making adjustments to optSensByBatesFFT settings, such as CharacteristicFcnStep, LogStrikeStep, NumFFT, DampingFactor, and so on. Note that if (LogStrikeStep * CharacteristicFcnStep) is 2*pi/ NumFFT, FFT is used. Otherwise, FRFT is used.

Strike = []; % Strike is not specified (will use the entire FFT or FRFT strike grid) [Delta, Kout] = optSensByBatesFFT(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta", 'NumFFT', NumFFT, ... 'CharacteristicFcnStep', 0.065, 'LogStrikeStep', 0.001); % Compare with numerical integration method Strike = Kout(Range); DeltaFFT = Delta(Range); DeltaNI = optSensByBatesNI(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, V0, ... ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta"); Error = abs(DeltaFFT-DeltaNI); table(Strike, DeltaFFT, DeltaNI, Error)

ans=7×4 table

Strike DeltaFFT DeltaNI Error

______ ________ _______ __________

79.76 0.57037 0.57037 6.3042e-09

79.84 0.56793 0.56793 7.156e-09

79.92 0.56548 0.56548 7.975e-09

80 0.56303 0.56303 8.7573e-09

80.08 0.56057 0.56057 9.4992e-09

80.16 0.55811 0.55811 1.0197e-08

80.24 0.55564 0.55564 1.0847e-08

% Save the final FFT (or FRFT) strike grid for future reference. For % example, it provides information about the range of Strike inputs for % which the FFT (or FRFT) operation is valid. FFTStrikeGrid = Kout; MinStrike = FFTStrikeGrid(1) % Strike cannot be less than MinStrike

MinStrike = 47.9437

MaxStrike = FFTStrikeGrid(end) % Strike cannot be greater than MaxStrikeMaxStrike = 133.3566

Compute the Option Sensitivity for a Single Strike

Once the desired FFT (or FRFT) settings are determined, use the Strike input to specify the strikes rather than providing an empty array. If the specified strikes do not match a value on the FFT (or FRFT) strike grid, the outputs are interpolated on the specified strikes.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 6); Strike = 80; Delta = optSensByBatesFFT(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta", 'NumFFT', NumFFT, ... 'CharacteristicFcnStep', 0.065, 'LogStrikeStep', 0.001)

Delta = 0.5630

Compute the Option Sensitivities for a Vector of Strikes

Use the Strike input to specify the strikes.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 6); Strike = (76:2:84)'; Delta = optSensByBatesFFT(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta", 'NumFFT', NumFFT, ... 'CharacteristicFcnStep', 0.065, 'LogStrikeStep', 0.001)

Delta = 5×1

0.6807

0.6234

0.5630

0.5011

0.4392

Compute the Option Sensitivities for a Vector of Strikes and a Vector of Dates of the Same Lengths

Use the Strike input to specify the strikes. Also, the Maturity input can be a vector, but it must match the length of the Strike vector if the ExpandOutput name-value pair argument is not set to "true".

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, [12 18 24 30 36]); % Five maturities Strike = [76 78 80 82 84]'; % Five strikes Delta = optSensByBatesFFT(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta", 'NumFFT', NumFFT, ... 'CharacteristicFcnStep', 0.065, 'LogStrikeStep', 0.001) % Five values in vector output

Delta = 5×1

0.6625

0.6232

0.5958

0.5748

0.5577

Expand the Outputs for a Surface

Set the ExpandOutput name-value pair argument to "true" to expand the outputs into NStrikes-by-NMaturities matrices. In this case, they are square matrices.

[Delta, Kout] = optSensByBatesFFT(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta", 'NumFFT', NumFFT, ... 'CharacteristicFcnStep', 0.065, 'LogStrikeStep', 0.001, ... 'ExpandOutput', true) % (5 x 5) matrix output

Delta = 5×5

0.6625 0.6556 0.6515 0.6483 0.6455

0.6222 0.6232 0.6239 0.6241 0.6238

0.5805 0.5900 0.5958 0.5996 0.6019

0.5381 0.5564 0.5674 0.5748 0.5798

0.4954 0.5225 0.5389 0.5499 0.5577

Kout = 5×5

76 76 76 76 76

78 78 78 78 78

80 80 80 80 80

82 82 82 82 82

84 84 84 84 84

Compute the Option Sensitivities for a Vector of Strikes and a Vector of Dates of Different Lengths

When ExpandOutput is "true", NStrikes do not have to match NMaturities. That is, the output NStrikes-by-NMaturities matrix can be rectangular.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 12*(0.5:0.5:3)'); % Six maturities Strike = (76:2:84)'; % Five strikes Delta = optSensByBatesFFT(Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta", 'NumFFT', NumFFT, ... 'CharacteristicFcnStep', 0.065, 'LogStrikeStep', 0.001, ... 'ExpandOutput', true) % (5 x 6) matrix output

Delta = 5×6

0.6807 0.6625 0.6556 0.6515 0.6483 0.6455

0.6234 0.6222 0.6232 0.6239 0.6241 0.6238

0.5630 0.5805 0.5900 0.5958 0.5996 0.6019

0.5011 0.5381 0.5564 0.5674 0.5748 0.5798

0.4392 0.4954 0.5225 0.5389 0.5499 0.5577

Compute the Option Sensitivities for a Vector of Strikes and a Vector of Asset Prices

When ExpandOutput is "true", the output can also be a NStrikes-by-NAssetPrices rectangular matrix by accepting a vector of asset prices.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 12); % Single maturity ManyAssetPrices = [70 75 80 85]; % Four asset prices Strike = (76:2:84)'; % Five strikes Delta = optSensByBatesFFT(Rate, ManyAssetPrices, Settle, Maturity, OptSpec, ... Strike, V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'OutSpec', "delta", 'NumFFT', NumFFT, ... 'CharacteristicFcnStep', 0.065, 'LogStrikeStep', 0.001, ... 'ExpandOutput', true) % (5 x 4) matrix output

Delta = 5×4

0.4350 0.5579 0.6625 0.7457

0.3881 0.5124 0.6222 0.7120

0.3432 0.4670 0.5805 0.6763

0.3010 0.4223 0.5381 0.6390

0.2619 0.3789 0.4954 0.6002

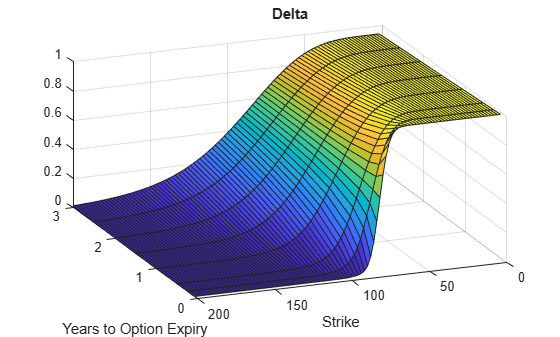

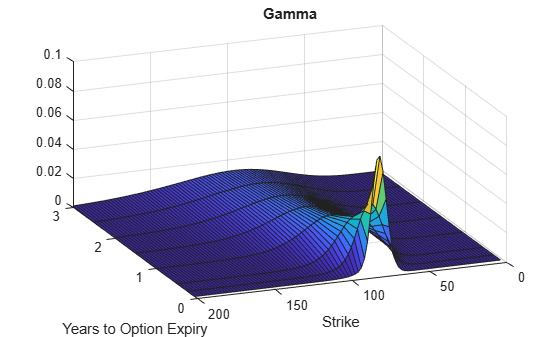

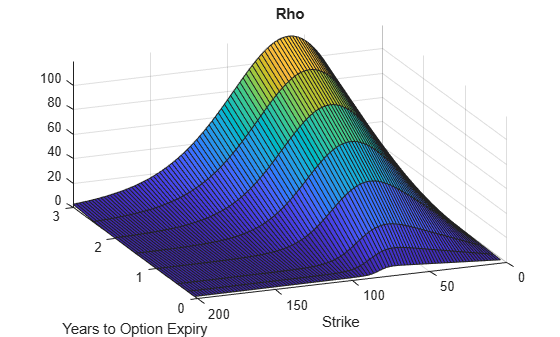

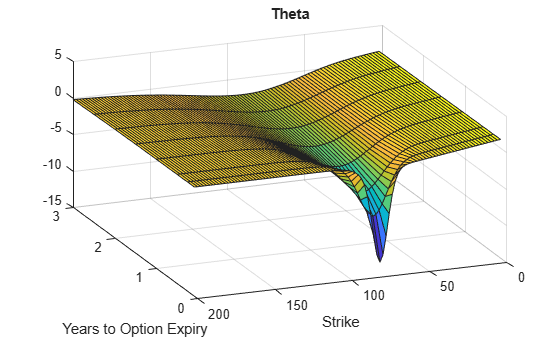

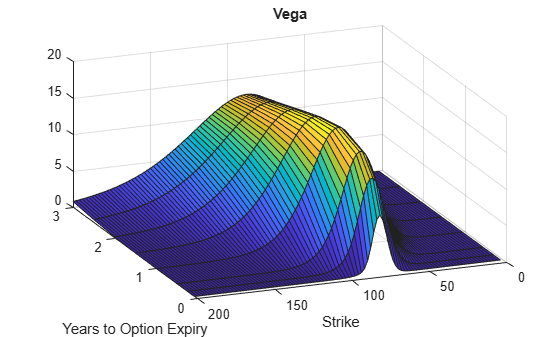

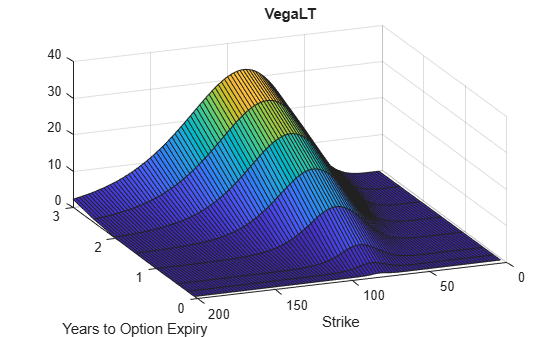

Plot Option Sensitivity Surfaces

Use the Strike input to specify the strikes. Increase the value for NumFFT to support a wider range of strikes. Also, the Maturity input can be a vector. Set ExpandOutput to "true" to output the surfaces as NStrikes-by-NMaturities matrices.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle, 12*[1/12 0.25 (0.5:0.5:3)]'); Times = yearfrac(Settle, Maturity); Strike = (2:2:200)'; % Increase 'NumFFT' to support a wider range of strikes NumFFT = 2^13; [Delta, Gamma, Rho, Theta, Vega, VegaLT] = optSensByBatesFFT(... Rate, AssetPrice, Settle, Maturity, OptSpec, Strike, ... V0, ThetaV, Kappa, SigmaV, RhoSV, MeanJ, JumpVol, JumpFreq, ... 'DividendYield', DividendYield, 'NumFFT', NumFFT, ... 'CharacteristicFcnStep', 0.065, 'LogStrikeStep', 0.001, ... 'OutSpec', ["delta", "gamma", "rho", "theta", "vega", "vegalt"], ... 'ExpandOutput', true); [X,Y] = meshgrid(Times,Strike); figure; surf(X,Y,Delta); title('Delta'); xlabel('Years to Option Expiry'); ylabel('Strike'); view(-112,34); xlim([0 Times(end)]);

figure; surf(X,Y,Gamma) title('Gamma') xlabel('Years to Option Expiry') ylabel('Strike') view(-112,34); xlim([0 Times(end)]);

figure; surf(X,Y,Rho) title('Rho') xlabel('Years to Option Expiry') ylabel('Strike') view(-112,34); xlim([0 Times(end)]);

figure; surf(X,Y,Theta) title('Theta') xlabel('Years to Option Expiry') ylabel('Strike') view(-112,34); xlim([0 Times(end)]);

figure; surf(X,Y,Vega) title('Vega') xlabel('Years to Option Expiry') ylabel('Strike') view(-112,34); xlim([0 Times(end)]);

figure; surf(X,Y,VegaLT) title('VegaLT') xlabel('Years to Option Expiry') ylabel('Strike') view(-112,34); xlim([0 Times(end)]);

Input Arguments

Name-Value Arguments

Output Arguments

More About

References

[1] Albrecher, H., Mayer, P., Schoutens, W., and Tistaert, J. "The Little Heston Trap." Working Paper, Linz and Graz University of Technology, K.U. Leuven, ING Financial Markets, 2006.

[2] Bates, D. S. “Jumps and Stochastic Volatility: Exchange Rate Processes Implicit in Deutsche Mark Options.” The Review of Financial Studies. Vol 9. No. 1. 1996.

[3] Carr, P. and D.B. Madan. “Option Valuation Using the Fast Fourier Transform.” Journal of Computational Finance. Vol 2. No. 4. 1999.

[4] Chourdakis, K. “Option Pricing Using Fractional FFT.” Journal of Computational Finance. 2005.

[5] Heston, S. L. “A Closed-Form Solution for Options with Stochastic Volatility with Applications to Bond and Currency Options.” The Review of Financial Studies. Vol 6. No. 2. 1993.